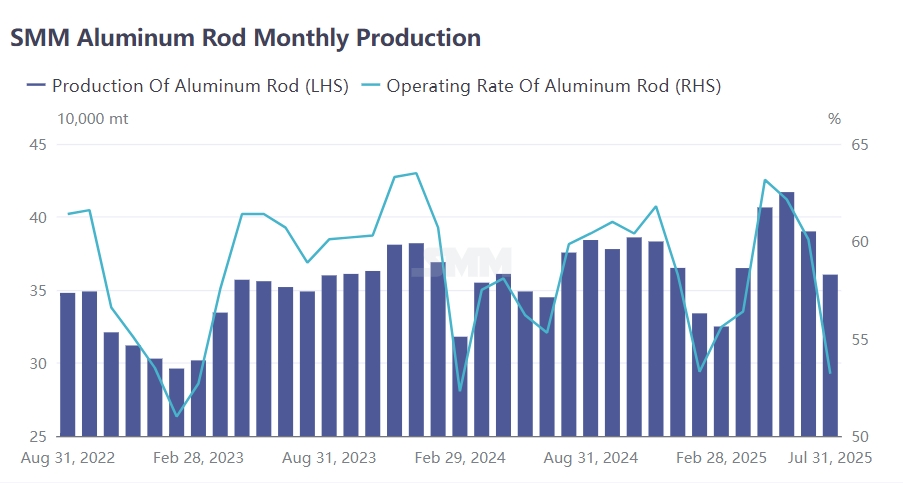

According to the latest monthly survey by SMM, China's total aluminum rod production in July 2025 reached 360,500 mt, down 29,600 mt from June. Against the backdrop of continuous aluminum rod capacity expansion, after excluding the impact of calendar days, the operating rate of aluminum rod plants in July was only 53.2%, down 6.89% MoM and 6.7% YoY. Under the triple pressures of accumulating in-plant inventory, sluggish downstream demand, and persistently high aluminum prices, aluminum rod plants were forced to implement production cuts and maintenance due to financial constraints, leading to a significant MoM decline in operating rates. However, since late July, the pullback in aluminum prices has loosened the price center, coupled with expectations of increased end-user cargo pick-up from August to September. Downstream consumption is expected to recover from the off-season, though current in-plant inventory at aluminum rod plants still requires time to digest. The supply-demand pattern for aluminum rods is projected to further improve in August.

Regionally, operating rates across provinces continued their downward trend in July. Shandong recorded a 76% operating rate, down 7 percentage points MoM, while Inner Mongolia saw a 72% rate, down 5 percentage points MoM. Henan's operating rate dropped 10 percentage points MoM, with Gansu and Guizhou experiencing declines exceeding 20 percentage points. Other regions also reported minor decreases. Both south China and northern markets exhibited exceptionally pronounced off-season sentiment in July, with operational financial pressures compelling enterprises to adopt production cuts and wait-and-see approaches. As August progresses, rigid demand is gradually recovering, and inventory destocking is expected to encourage plants to resume normal production pace. Provincial operating rates are anticipated to enter a slow recovery phase in August.

SMM believes that the aluminum rod market resumed normal consumption patterns in August. August marked the delivery period for the first batch of State Grid's ultra-high voltage projects in H1, and subsequent orders from State Grid are expected to enter the delivery phase gradually. Additionally, tenders from H1 will be progressively fulfilled in H2 and the first half of next year. It is projected that there will be at least one more industry-wide concentrated delivery cycle in H2, with aluminum rod consumption likely to receive support and a boost in September.